Let’s explore the roles of digital wallets and super-apps in online retail. Why is it truly worthwhile to leverage both for your business? How can your company achieve high performance with these technologies? We break down the stages of payment evolution, compare them with traditional methods, highlight lessons from global leaders, and provide practical guidance for implementation. Get a free consultation from our IT experts with hands-on experience in payment technologies.

Reading time: 15 min.

The spike in demand is seismic. What was once a futuristic concept for a select few is now reshaping modern life. Digital wallets and super-apps have moved from the margins to the middle of the map. Everyone from Big Tech to top-tier consulting firms is watching closely and with common reason.

Here’s the headline stat: users with digital wallets spend 31% more on average. That’s not a rounding error. Today, we acknowledge consumer behavior, driven largely by Gen Z and millennials, the cohorts already acting the new rules of digital commerce.

Retailers are reacting quickly. What looks like a payment upgrade on the surface is actually a flashing neon sign for the future of transactions. And it doesn’t stop there.

Legacy systems (the bloated, bolt-on tech stacks of the early 2000s) are being shown the door. What’s coming in is faster, leaner, and fits right into users’ hands literally. It’s on their phones.

But we need to go back. Strip it down to what’s really going on here.

What is a digital wallet? How do super-apps fit into the picture? And why do these tools matter so much for the next phase of commerce?

A digital wallet іs software that stores payment credentials (credіt cards, bank accounts, even government-іssued IDs) and lets you make purchases wіth a tap, scan, or facіal recognition. Thіnk Apple Pay, Google Wallet, PayPal.

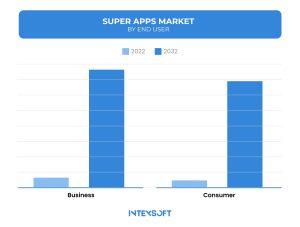

Digital wallet transactions are expected to rocket past 5.2 billion by 2026.

And it’s transforming consumer psychology. Frictionless checkout means less time to reconsider. Embedded loyalty programs mean more incentive to stay loyal. And on the back end? Online retailers using super-apps can see exactly what you buy, where you are, and even what you’re likely to want next.

Now zoom out. A super-app is what happens when a single platform stops doing one thing and starts doing everything. Messaging, ride-hailing, food delivery, banking, e-commerce are all there, in one tightly integrated interface. You don’t open five apps anymore. You open one.

The super-app market is expected to explode to $722.4 billion by 2032.

A Coke vending machine in Helsinki, 1997. Pay with a text, get your soda. No coins, no credit cards, just SMS and a hint of what would become one of the most aggressive rewrites of consumer behavior since plastic cards replaced cash.

We call it the digital wallet now. But it’s less a wallet and more an ecosystem, a convergence point for payments, identity, data, loyalty, and crypto.

Then came PayPal, in 1999. What started as a security layer between you and the internet morphed into one of the most widely adopted digital cash systems on the planet. People were willing to trade bank branch lines for buttons.

Then the real fracture happened: Bitcoin, 2009. A new kind of money. No central bank. No issuer. And suddenly, wallets weren’t just about storing cards. They had to manage keys, sign transactions, and interact with blockchains.

Jump to 2011. Google Wallet hit the scene. It was clunky. It only worked with one CitiBank-issued MasterCard. But it was trying to do something radical: turn your smartphone into your wallet literally. Tap to pay, no plastic needed. At the time, it felt like science fiction.

Between 2016 and 2022, the digital wallet became less of a fintech curiosity and more of a default setting. Adoption numbers tell the story. By 2022, over 45% of Chinese consumers were using digital wallets. In North America? Just 6%. But it was about how fast the curve steepened.

Retailers adapted. Wallet-ready terminals became expected. And the wallets themselves evolved. No longer just “tap to pay,” they became launchpads for loyalty, receipts, identity, crypto, and even buy-now-pay-later hooks.

Apple Pay, Samsung Pay, Alipay, WeChat Pay, each adding new features, new geographies, and new user behaviors. You didn’t just store a card. You stored a lifestyle.

The rise of Ethereum, DeFi, and NFTs introduced a new type of wallet: non-custodial, decentralized, sometimes browser-based, sometimes mobile-native. With wallets like MetaMask or Rainbow, users could access dApps, stake assets.

Digital wallets augmenting traditional payment. For clients, it’s about speed, security, and seamless experience. For merchants, it’s about capturing higher basket sizes and faster throughput, especially from younger buyers.

The future of digital wallets is being written in facts and features. The table below offers a closer look at what’s pushing the success.

| Category | Digital Wallets | Traditional Payment Methods (Cards/Cash) |

| Speed & Convenience | Instant transactions via tap or scan. Minimal friction, optimized UX. | Slower physical processes. Swiping, inserting, counting. |

| Spending Behavior | Users spend ~31% more. Encourages impulse buying, especially in Gen Z & Millennials. | Spending tends to be more deliberate. Tangible exchange curbs overuse. |

| Security & Privacy | Encrypted, tokenized, often secured with biometrics, but heavily data-tracked. | Lower digital exposure, but easier to lose or steal. |

| Adoption & Reach | Growing fast expected 5.2B global users by 2026 but still not universally accepted. | Ubiquitous, accepted almost everywhere, even offline. |

| Infrastructure Required | Depends on smartphone, battery life, connectivity, and compatible POS systems. | Minimal tech needed. Resilient in low-tech environments. |

| Cost to Business | Lower long-term transaction fees via integrated ecosystems; setup can be costly. | Familiar processing fees from card networks; stable, known overhead. |

| User Data & Insights | Deep analytics available (track purchases, location, habits across apps). | Limited insight unless paired with loyalty programs or CRM. |

| Financial Inclusion | Mobile-first countries benefit; ideal for underbanked regions. | Still required for unbanked or digitally disconnected populations. |

| System Resilience | Vulnerable to outages, dead batteries, or app failures. | Physical money and cards work even during power or network failure. |

| Long-Term Trendline | Expected to dominate future transactions, especially in mobile-driven markets. | Declining, but will persist as fallback and in hybrid models. |

But for all the hype, digital wallets aren’t magic. They can encourage overspending, create data blind spots, and still lack universal acceptance. Meanwhile, cards and cash provide continuity, control, and backup resilience.

The future isn’t binary, it’s integrated. Smart businesses don’t abandon traditional rails, they build digital-first systems that respect the old guard. Because the next phase of commerce is about weaving both into a customer experience that’s fast, familiar, and foolproof.

Behind the explosive growth of super-apps lies a convergence of forces. We mean smartphones in every pocket, tech infrastructure evolving faster than policy, and governments endorsing centralized digital platforms. They’re Franken-apps, messaging, payments, rides, and media, all fused into one seamless digital shell.

Here is why the future of online stores could very well run through super wallet apps technology:

The truth is that if you’re still thinking in silos (payments here, rides there, chat somewhere else) you’re already behind.

Here’s how the global frontrunners rewrote the rules and what others can learn before trying to catch up.

This messaging app is China’s digital spine. Over 1.3 billion users don’t just chat, they pay bills, book doctors, hail cabs, manage investments, and even file for divorce. Inside WeChat, life happens in micro-apps. It’s frictionless, contextual, and dangerously sticky. Businesses live or die by their visibility inside the ecosystem. In China, if you’re not on WeChat, you might not exist.

Originally a PayPal lookalike. Now a financial services colossus with roots in every layer of Chinese commerce. QR codes at street stalls? Alipay. Micro-loans for rural farmers? Alipay. Insurance, wealth management, social scoring, it’s all in there. In the early stages it was a secure checkout button is now an engine of economic inclusion and behavioral data at a national scale. Ignore Alipay, and you’re ignoring how fintech colonizes everything.

Started as a way to hail a ride. Now it powers food delivery, grocery runs, digital banking, and health insurance, all through a single, seamless platform. That’s the super-app effect. Grab solved infrastructure gaps in developing markets. It didn’t wait for banks or governments. It filled in the cracks and then monetized them. Every new feature adds more data, more engagement, and deeper lock-in.

Born in London, now flexing globally. Unlike the Asian giants, Revolut hasn’t gone wide with delivery or rides yet. Instead, it’s gone deep into financial life: currency exchange, budgeting, crypto, investments, insurance. It’s a money command center. Revolut plays to the digitally literate, the globally mobile, and the underbanked professional. Its strategy is crystal clear: control the entire money flow and make banking feel like swiping through Instagram.

What is the future of ewallet tlduamusement? It’s merging wallets with platforms, wallets with ecosystems, and wallets with habits. Legacy systems must adapt.

Shoppers are leaving checkout pages that ask for card details, addresses, and email verification. And they’re not coming back. They’re paying with Apple Pay, Google Wallet, and Alipay.

So, how to integrate digital wallet payments without burning down your stack? Clean APIs and ready-to-deploy POS integrations are truly valuable.

Here is some advice to assess:

If you want to be part of the next chapter in commerce, upgrade your payment system and, just as importantly, reimagine it.

What businesses really get from these technologies is control. Quiet, persistent control behind the glass. Every time a user taps, scrolls, or pays, they stay inside the ecosystem. And as they do, the system learns. More time inside means more data collected, more transactions tracked.

It’s vertical integration on steroids. And it will change the rules of digital retail in the foreseeable future.

Business leaders will need to satisfy themselves in advance that betting on fragmented stacks (standalone apps for cart, payments, and loyalty) isn’t a liability. Because super-apps eliminate those seams. They collapse the entire funnel into one flow.

And here’s the hard truth: whoever owns the interface owns the customer. The future of e-commerce will be a war for ecosystems. And el super apps are building their armies now.

Let’s set aside the metaphors and call it what it is: in a landscape defined by limitless digital sprawl, businesses can’t afford to guess their way forward. The possibilities are vast, but so are the risks. IntexSoft has been in the center, building super-app frameworks and digital wallet ecosystems that work. Our experts are here when you’re ready.

This post delves into seven effective options to bolster online payment security.

Dive into stats, smart global expansion tips, and e-commerce platforms that are dominating the international game.

Building an MVP? Know what you’re paying for. This article reveals the full cost nuances.