Starting a new business? Minimum Viable Traction gets you ready to raise capital. Learn which metrics matter, how AI is reshaping investor expectations, and the pitfalls that keep startups from reaching MVT. Think you measure up? Let’s find out. Book your complimentary IntexSoft Startup Diagnostic.

Reading time: 18 min.

As investor Bruce Cleveland argues, a product alone is not proof of a business. If it were, 80-85% of early-stage startups (and up to 94% in consumer markets) would not disappear while trying to bridge the Traction Gap between an Initial Product Release and Minimum Viable Traction. The real challenge is to prove that demand exists, customers keep coming back, and growth can be reproduced on demand.

This is the threshold where the MVT startup concept becomes truly relevant.

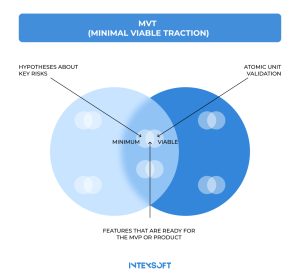

MVT has one job: eliminate risk around your most critical assumptions. Rather than building dozens of features, founders focus on validating a single atomic unit of value: the lowest-hanging fruit capable of proving demand.

That unit differs from one business to another. For Airbnb, it was a booking. For Uber, it was a ride. For Stripe, it was a successful payment.

Founders who validate the core unit of value before expanding the product can compress years of uncertainty into months, with some serial entrepreneurs reaching a $1M revenue run rate within their first six months.

Founders often treat MVT as another form of MVP, creating the dangerous illusion that shipping a product and creating a business are the same thing. They are not. (Our diagram above illustrates the difference.)

A Minimum Viable Product (MVP) answers a technical question: “Can we build it?”

Minimum Viable Traction answers the question that determines whether a startup can survive once the early excitement wears off: “Can we sell it repeatedly, predictably, and at a profit?”

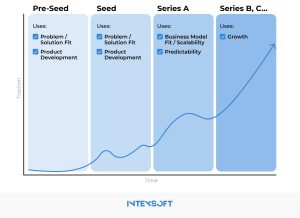

Reaching MVT indicates that your company has crossed a major threshold: the startup has achieved multiple consecutive quarters of sustainable growth and demonstrated that its product has earned real market acceptance. By then, uncertainty has shifted from viability to execution. The startup has already built repeatable sales and marketing processes, and leadership can scale systematically with a clear understanding of Customer Acquisition Cost (CAC) and Lifetime Value (LTV).

As companies mature, investor expectations shift from potential to proof. While the exact numbers vary by business model, the underlying logic remains the same. Although IntexSoft cannot guarantee identical results, you can compare your performance against the following MVT-level traction benchmarks venture investors typically look for:

| Business Model | Primary Startup Traction Metrics | Critical Focus Area |

| B2B SaaS | $500K MRR | Predictable conversion rates |

| Marketplaces | Monthly transaction volume and net revenue growth | Take rate, liquidity density & retention |

| B2C | ~25,000-100,000 daily active users | Rapidly decreasing CAC |

| General | 8-12 consecutive quarters of sustained growth, steadily up and to the right | Validated GTM & Cohesive Team |

The benchmark to beat is $500K in Monthly Recurring Revenue (MRR). If you are still well below that number, the company may already have early repeatability, but it has not yet reached the scale where investors can treat that repeatability as durable. That’s the level you’re still working to master.

In IntexSoft‘s experience, reaching MVT from this stage typically requires tripling the business over the following 12-18 months. Yet revenue alone does not define success. Among the most important traction metrics for SaaS startups is the ability to attract new customers with predictable conversion rates.

Being a marketplace does not lower the bar. The benchmark should be tied to monthly transaction volume, net revenue, take rate, and liquidity density, not SaaS-style recurring revenue. The challenge is that every dollar must first flow through the platform’s take rate, making commission economics one of the core drivers of marketplace traction.

Investors also demand proof of liquidity. That means cohort repurchase rates of 40% to 60% within 90 to 180 days. Equally important is transaction density high enough to prove that activity is concentrated and difficult to disrupt.

And remember, for marketplaces, depth beats breadth. One niche market that works reliably is more valuable than seven niche markets that are barely moving because it proves liquidity.

Many investors consider 1 million active users a milestone for consumer apps. But in many cases, 25,000-100,000 highly engaged people can already be enough to show early traction. Audience size matters, but acquisition efficiency matters just as much. The business must also demonstrate that it can bring Customer Acquisition Cost (CAC) down quickly. For most B2C startups, uncontrolled marketing spend is the difference between scaling and running out of capital.

In social apps, retention is everything. Consider user stickiness, measured by how many monthly users come back every day. Think of a messaging app people check throughout the day or a navigation app they open every morning before leaving home. “I just open it automatically” is exactly the behavior you’re looking for. If roughly one in four to one in two monthly users returns every day, it’s a strong sign that the product has become part of their routine.

Few product-market fit signals are as convincing as strong waitlist momentum. Ideally, it should grow by more than 10% week over week without relying heavily on paid marketing.

At IntexSoft, business analysts also track engagement, downloads, and product usage as important indicators. But indicators are not what investors ultimately buy into. The factor that mattered yesterday, matters today, and will matter tomorrow is sustained, consistent startup growth quarter after quarter.

MVT also needs to be backed by qualitative strengths: rapid product iteration, a proven and predictable go-to-market (GTM) strategy, and a cohesive team that can effectively hire, develop, and retain talent.

Only after reaching these metrics – and this point bears repeating – can you say that the company’s GTM engine has been fully validated by the market. From that point forward, the MVT startup must meet the much tougher expectations of late-stage capital. That means growing recurring yearly revenue from $6 million to $18 million over the next year, then continuing to double it in the following years on the path to a successful exit.

IntexSoft places special emphasis on Burn Multiple. If growth disappeared tomorrow, how much of it was actually bought? Burn Multiple answers that question by revealing the true cost of recurring revenue expansion.

For founders asking how much traction do investors expect, Burn Multiple is often one of the first metrics investors look at. To calculate it, divide net burn by net new ARR over the same period.

What does a Burn Multiple below 1.5x actually mean in the eyes of investors? And when does expansion cross the line into artificial territory?

Of course, with 2027 already around the corner, no serious startup discussion is complete without addressing AI automation. Today, the market increasingly separates AI-native companies from the rest of the field. According to an article by Colin Gardner of Yonder VC, firms in this category routinely attract capital at valuation premiums that average roughly 30-50% above comparable startups. But that premium comes with a tradeoff: investors expect stronger startup growth metrics and more convincing proof of Minimum Viable Traction before writing a check.

They closely evaluate Annual Recurring Revenue (ARR) per employee. For private SaaS startups, the benchmark today is roughly $130,000. AI-based startups, however, are held to nearly twice that standard. Because automation allows them to run with minimal headcount, capital allocators want them to generate disproportionately higher revenue per employee.

If an AI-native startup is your chosen path, sooner or later you will face a question like this: “What happens to your traction if OpenAI makes your core feature available by default?”

You should have a well-prepared answer. Traction before fundraising must be built on proprietary data and complex workflows, not merely on calls to flexible APIs.

Now look at Burn Multiple from the perspective of an MVT AI startup. The emergence of new technologies is forcing investors to rethink what efficient growth looks like. A Burn Multiple between 0.8x and 1.2x, combined with strong Retention Rates, is rapidly becoming the new benchmark. These are real operating metrics. Measured against them, traditional SaaS companies with high operating costs often appear a generation behind, including at the MVT stage.

What makes this possible is a structural advantage. AI startups can automate substantial portions of both product development and customer support. At the Minimum Viable Traction stage, this means burning less than one dollar of investor capital for every new dollar of revenue created.

As we noted at the beginning of this article, roughly 80-85% of early-stage companies fail while trying to cross the Traction Gap, the startup equivalent of the Valley of Death, not because of technology, but because they fall into the same three traps.

Waitlists, free downloads, traffic spikes, and social media likes can make a startup look successful. Investors know better. None of these metrics tell you whether customers are willing to pay. And without paying customers, they reveal very little about the true health of your startup.

The average journey from Seed Funding to Series A now stretches to roughly 616 days. Many startup founders begin raising their next major round from a position of weakness, with shrinking runway and metrics that have yet to prove the business.

The smarter strategy is to use bridge funding to buy time. Within a disciplined startup validation framework, a well-timed bridge round gives founders the runway needed to reach MVT before returning to the market. This preserves negotiating leverage. It also helps ensure that the next round is raised on the strength of validation rather than the pressure of a shrinking bank account.

The pursuit of multiple distribution channels rarely accelerates traction. What it reliably accelerates is cash burn. IntexSoft believes the path to MVT starts with focus: pick one acquisition channel, master it, and demonstrate that it can deliver repeatable growth before moving on to the next one.

MVT comes from validation first and scale second.

Use this checklist to identify the strongest signs of startup traction and compare your progress against real minimum viable traction examples.

To compete for top-tier venture capital, your startup must outgrow founder-led execution. Systems, Team, Product, and Revenue should already run on repeatable processes built for rapid scale.

Thinking about upgrading to a smart office automation system? This article includes everything you need to know.

This article explains the challenges and benefits of CRM MVP development, outlines key steps, and shares a real-life success story.

We’ve explored the MVP landscape from multiple angles.